One of the strengths of EDS, given our platform was born out of the buyside, is the ability to spot developing “change” and quickly put the upside or downside into context.

In this Issue:

Case Study on Akamai Technologies (AKAM)

Akamai has been a volatile stock over the past 5 years, both creating and destroying wealth for many investors. However, given its early entry as a leading Internet company, it has maintained strong margins for many years, peaking at over 40%, on sales growth in the double-digits. Over the past 3 years, though, margins and growth have been on a steady march downward, with stock under-performance and volatility following growth. One of the strengths of EDS, given our platform was born out of the buyside, is the ability to spot developing “change” and quickly put the upside or downside in context, including whether others are starting to notice the same “change”. In October 2017, AKAM was upgraded by Guggenheim, and we wanted to quickly see if additional work on Akamai was warranted.

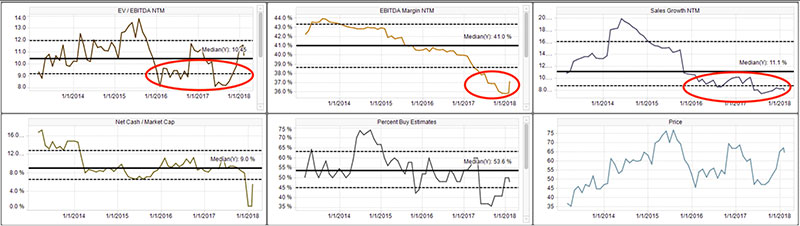

AKAMAI FUNDAMENTAL TIME-SERIES ANALYSIS

Figure 1. At the time of the upgrade, the AKAM valuation was at multi-year lows, likely meaning the investment community expected the trend of lower sales and margins to continue. However, we can clearly see sales growth has been bottoming. Now the question is....How much should I focus on sales growth or is another metric more important?

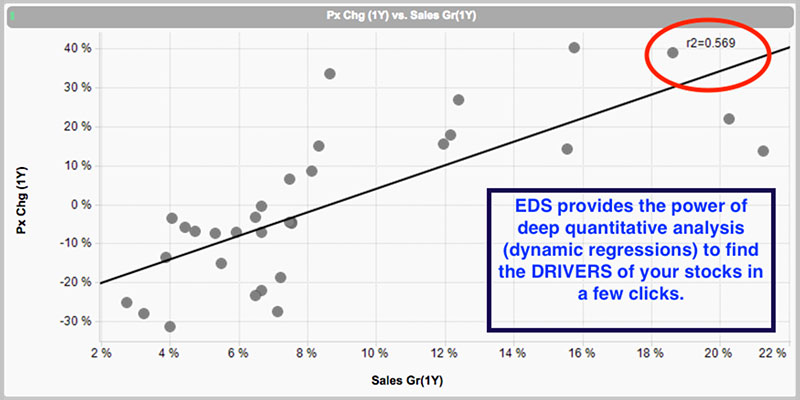

By regressing multiple factors and time-periods against the stock price, we quickly note that sales has the best fit (57%) to the stock price... So YES, paying attention to sales growth is important.

AKAMAI DYNAMIC REGRESSION (STOCK PRICE AND SALES)

If our Working Thesis is:

- Sales are bottoming in the 8% range.

- EBITDA Margins are stable in the 36% range.

Before I spend too much time researching the idea, What is my Upside? After all, Akamai is now a different company, more akin to a monopoly with high-margins and low growth.

Question we need to answer?

How are other technology companies with high margins and low growth valued?

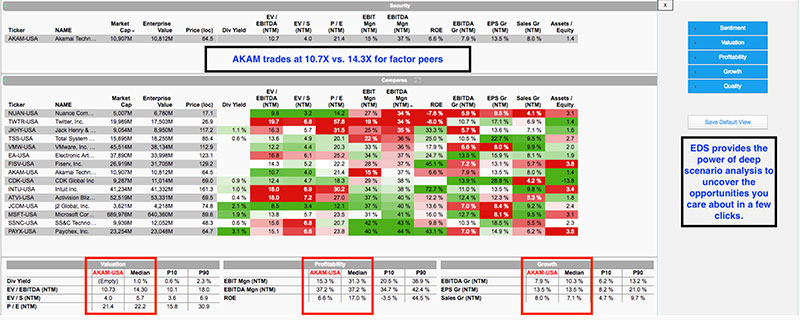

EDS DYNAMIC COMP SHEET + SCENARIO ANALYSIS

Figure 2. Other technology companies, with similar margins (37%) and growth (7.1%) are valued much higher, at over 14X EV/EBITDA and 5X Sales, providing significant upside to AKAM if our thesis plays out.

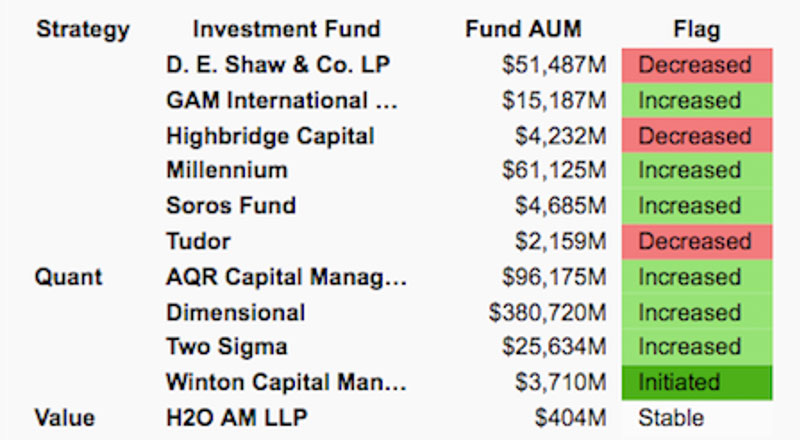

Another Question that Interests us? While the upside looks significant, we are interested if others have started to “sniff” this out...

Given the large disparity between the current valuation of Akamai and other similar companies,

Quant funds have taken notice....

If you are interested in a demo or have any questions please reach out to us at sales@equitydatascience.com.