The evolution of big data has become a necessity in the fundamental investor world, with hedge funds and asset managers alike searching for a multitude of ways to utilize the plethora of data consumed and gain the insights that will help drive better outcomes. While each have their own secret sauce, without the right data coupled with modernized, configurable technology to help dissect and draw those “aha” moments for next best action, it’s too easy to fall behind.

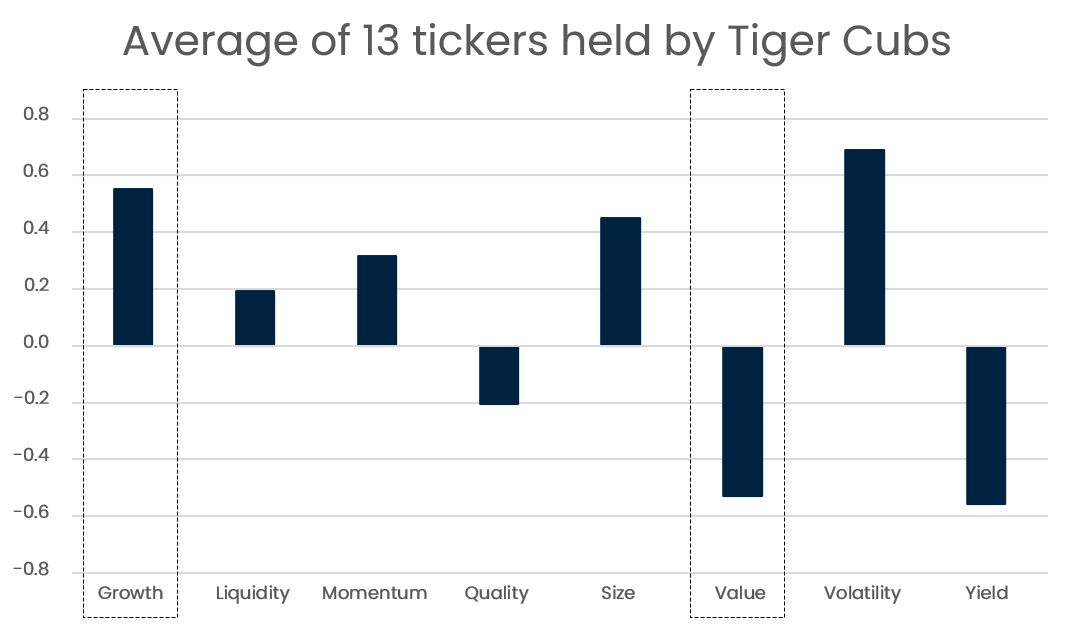

Here's one way to leverage the data. We took the 40+ identified Tiger cubs on EDS and filtered their portfolios with two criteria.

- All names held by at least five cubs

- Median fund position in the name was at least 1%

The resulting portfolio average of 13 names clearly showed a positive growth and negative value bent. Along with those expected exposures, this portfolio average also exhibited high volatility and negative yield.

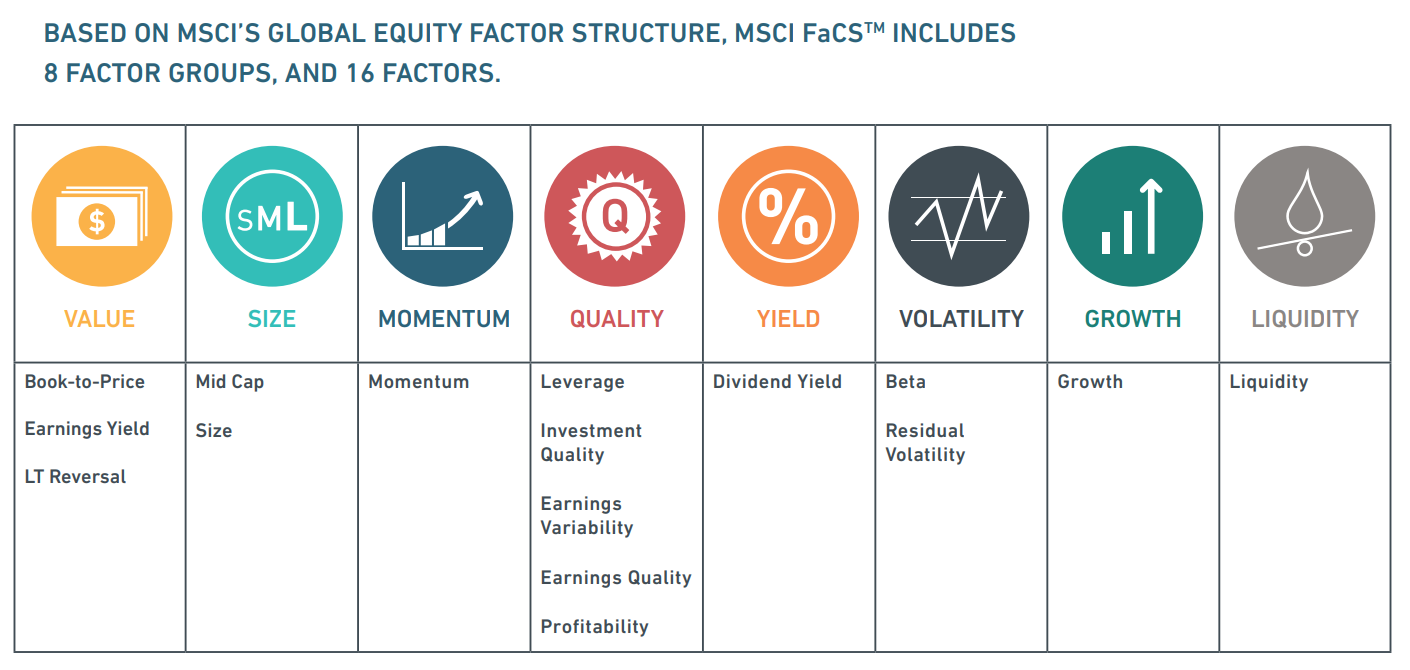

The factors used in the calculations of these eight factor groups sourced from MSCI:

Now, if you were to look at the performance of these eight factor groups YTD (until 03/11/22), you can see that Value and Yield (the factors this mock portfolio is most negatively exposed to) have been the best performing factors YTD while Growth and Volatility (the factors the mock portfolio is positively exposed to) have underperformed. Though the returns seem relatively small in magnitude, the data shown are from pure factor portfolios so you have to pay attention to the themes and trends of these exposures and consider the impact made. They help understand why the stocks are moving the way they are, and therefore can be more precise on what you’re betting on.

In a rising rate environment, investors would have typically expected to see Value outperform Growth. However, the underperformance of higher beta and crowded names (captured by the Volatility factor) has led to a significant underperformance of this mock portfolio.

This equal weighted portfolio was down 20% YTD (as of 03/11/22), underperforming the S&P 500 by more than 700 bps. Shown below, we have run this portfolio on our factor return attribution module and can draw some interesting conclusions.

- Specific return (or alpha) contribution (outlined in blue) was a mere -136bps.

- Majority of the negative return for this portfolio was because of factor (or beta) contribution. You can see the breakdown of the -18.31% factor contribution (outlined in red) by stock and also by factors and factor groups.

- The outsized exposure to Software (both Internet Software and IT Services) resulted in a -271 bps contribution (outlined in yellow) to the portfolio.

Asset allocators are increasingly asking their fund managers to produce evidence of superior stock picking and even holding them to specific risk and return requirements. How do these stack up against your portfolio? We can help you understand your exposures and returns. We could even run your portfolio in our Portfolio PNL page to help you analyze your return stream, and in turn understand where the dangers in your portfolio could be hidden. Contact us here and let us know how we can help.